How Age Affects Premiums for Critical Illness Insurance

So, here’s the deal. We’re living in a time when everyone’s concerned with health and fitness. People are devouring protein, hitting the gym and tracking their steps as if it’s a full-time job. But here’s the kicker — despite all that, the incidence rate of critical illness like cancer, stroke, organ failure is only increasing. And what is even more worrying is that Indians are getting these diseases at much younger ages than in the past. And being outwardly fit and rich is also no protection against this, as we have seen with movie stars and entrepreneurs. Crazy, right? Which is why these days you need to get a good health insurance plan for yourself and the family. But here’s something we would like to bring to your attention. Your normal health insurance plan can cover the cost of hospitalization and maybe even some expenses after that. But critical illness recovery can run into months and sometimes even years. The changes in your lifestyle can be permanent in nature. What about the loss of not being able to work for six months’ post cancer surgery? Who will cover the cost of not being able to do a high-stress job after a heart attack?

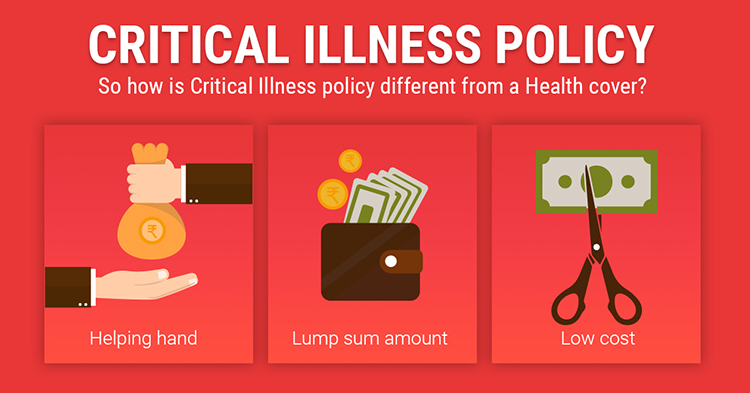

So enter critical illness insurance. This is the booster to your normal health insurance. It’s an add-on — or in some cases, a standalone insurance policy — that provides you with additional coverage for things like heart attacks, strokes or cancer. If you ever get one of these, the plan pays you a lump sum to help pay for costs that your regular insurance may not cover. Consider it a money safety net when life takes a turn.

So, when do you need critical illness insurance?

Actually, there’s no “perfect” age for any insurance and circumstances of individuals vary, but here’s the brief decision frame:

In your 20s and 30s: Now is a good time to start planning. You’re younger, likely healthier, and premiums cost less. Plus, it’s intelligent to secure coverage ahead of time, before any health problems arise.

In your 40s and 50s: Don’t miss this! As you age, the risk of a critical illness only increases. If you haven’t already, now is the time to prioritize critical illness insurance.

What do you need to know before you Critical Illness Insurance?

Your Age and Health: The younger and healthier you are at a time of purchase, the better. You’ll pay less for coverage, and it’s easier to get approved in underwriting. If you’re in your 20s in your 30s, you’re better off getting a critical illness policy in addition to your health insurance. If you’re older, don’t leave it as optional — make it a requirement.

Affordability: Can you afford the premiums? If you are in your 20s or 30s and money is tight, it’s O.K. to let it wait, but make a plan to get it later on. By your 40s or 50s, you will hopefully have more savings to funnel toward this type of coverage.

Family History: If your family has a history of illnesses, including cancer or heart disease, don’t wait. Buy a critical illness policy early to protect yourself from the possibility of.

Your Job and Lifestyle: If you are in a high-stress job or lead a high-stress life, it’ll pay to get critical illness insurance earlier. Stress can play havoc with your health and critical insurance can help you be prepared.

Your Coverage Needs: Have dependents or large financial obligations to protect? A critical illness policy provides an additional layer of protection for you and your family.